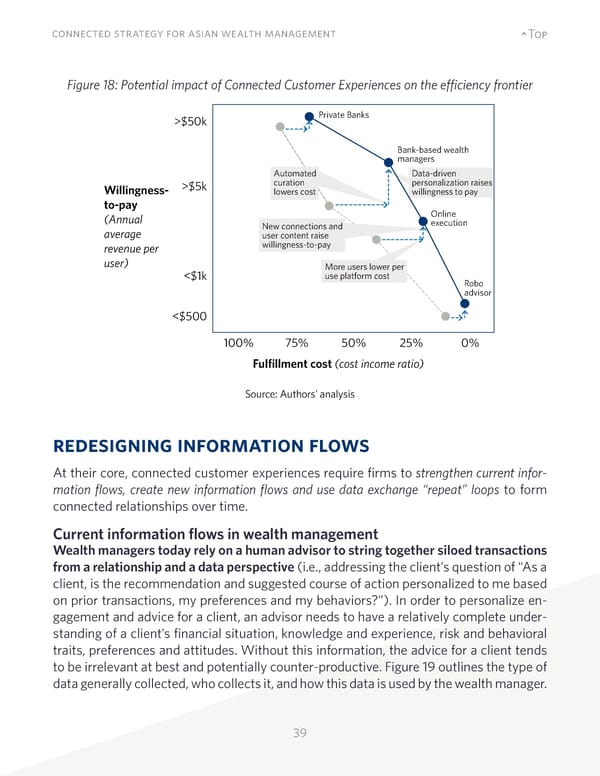

39 connected strategy for asian wealth management ^Top Figure 18: Potential impact of Connected Customer Experiences on the efficiency frontier redesigning information flows At their core, connected customer experiences require firms to strengthen current infor- mation flows, create new information flows and use data exchange “repeat” loops to form connected relationships over time. Current information flows in wealth management Wealth managers today rely on a human advisor to string together siloed transactions from a relationship and a data perspective (i.e., addressing the client’s question of “As a client, is the recommendation and suggested course of action personalized to me based on prior transactions, my preferences and my behaviors?”). In order to personalize en- gagement and advice for a client, an advisor needs to have a relatively complete under- standing of a client’s financial situation, knowledge and experience, risk and behavioral traits, preferences and attitudes. Without this information, the advice for a client tends to be irrelevant at best and potentially counter-productive. Figure 19 outlines the type of data generally collected, who collects it, and how this data is used by the wealth manager. $50k 100% 75% 50% 25% 0% Private Banks Fulfillment cost (cost income ratio) Willingness- to-pay (Annual average revenue per user) Bank-based wealth managers Online execution Robo advisor More users lower per use platform cost New connections and user content raise willingness-to-pay Data-driven personalization raises willingness to pay Automated curation lowers cost Source: Authors' analysis

Connected Strategy for Asian Wealth Management Page 38 Page 40

Connected Strategy for Asian Wealth Management Page 38 Page 40