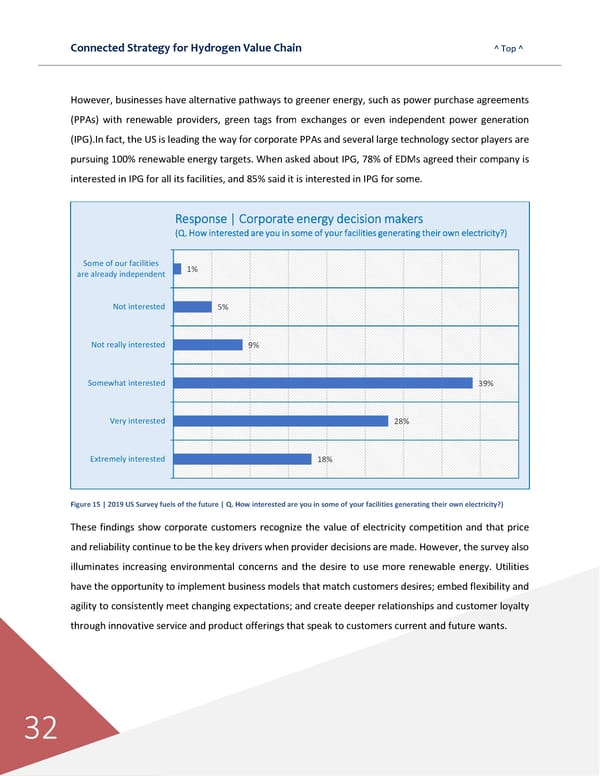

Connected Strategy for Hydrogen Value Chain ^ Top ^ 32 However, businesses have alternative pathways to greener energy, such as power purchase agreements (PPAs) with renewable providers, green tags from exchanges or even independent power generation (IPG).In fact, the US is leading the way for corporate PPAs and several large technology sector players are pursuing 100% renewable energy targets. When asked about IPG, 78% of EDMs agreed their company is interested in IPG for all its facilities, and 85% said it is interested in IPG for some. Figure 15 | 2019 US Survey fuels of the future | Q. How interested are you in some of your facilities generating their own electricity?) These findings show corporate customers recognize the value of electricity competition and that price and reliability continue to be the key drivers when provider decisions are made. However, the survey also illuminates increasing environmental concerns and the desire to use more renewable energy. Utilities have the opportunity to implement business models that match customers desires; embed flexibility and agility to consistently meet changing expectations; and create deeper relationships and customer loyalty through innovative service and product offerings that speak to customers current and future wants. 18% 28% 39% 9% 5% 1% Extremely interested Very interested Somewhat interested Not really interested Not interested Some of our facilities are already independent Response | Corporate energy decision makers (Q. How interested are you in some of your facilities generating their own electricity?)

Connected Strategies for the Hydrogen Value Chain Page 32 Page 34

Connected Strategies for the Hydrogen Value Chain Page 32 Page 34