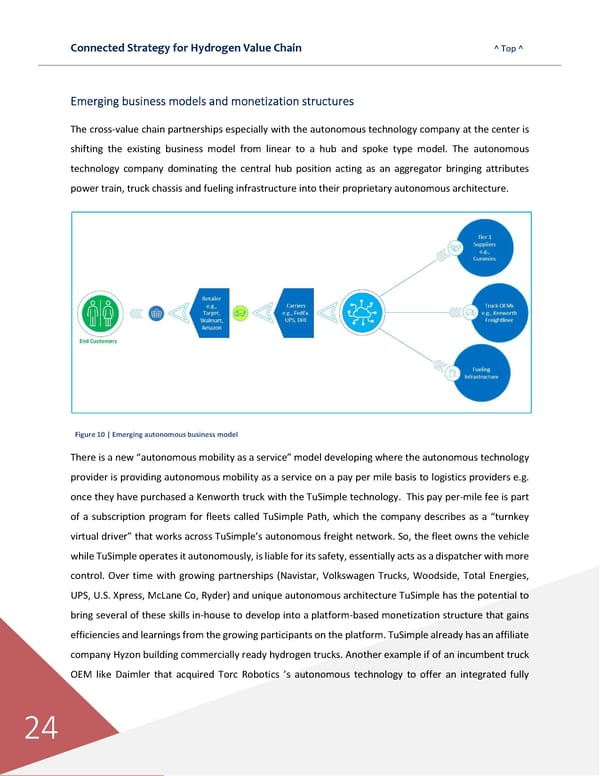

Connected Strategy for Hydrogen Value Chain ^ Top ^ 24 Emerging business models and monetization structures The cross-value chain partnerships especially with the autonomous technology company at the center is shifting the existing business model from linear to a hub and spoke type model. The autonomous technology company dominating the central hub position acting as an aggregator bringing attributes power train, truck chassis and fueling infrastructure into their proprietary autonomous architecture. Figure 10 | Emerging autonomous business model There is a new “autonomous mobility as a service” model developing where the autonomous technology provider is providing autonomous mobility as a service on a pay per mile basis to logistics providers e.g. once they have purchased a Kenworth truck with the TuSimple technology. This pay per-mile fee is part of a subscription program for fleets called TuSimple Path, which the company describes as a “turnkey virtual driver” that works across TuSimple’s autonomous freight network. So, the fleet owns the vehicle while TuSimple operates it autonomously, is liable for its safety, essentially acts as a dispatcher with more control. Over time with growing partnerships (Navistar, Volkswagen Trucks, Woodside, Total Energies, UPS, U.S. Xpress, McLane Co, Ryder) and unique autonomous architecture TuSimple has the potential to bring several of these skills in-house to develop into a platform-based monetization structure that gains efficiencies and learnings from the growing participants on the platform. TuSimple already has an affiliate company Hyzon building commercially ready hydrogen trucks. Another example if of an incumbent truck OEM like Daimler that acquired Torc Robotics ’s autonomous technology to offer an integrated fully

Connected Strategies for the Hydrogen Value Chain Page 24 Page 26

Connected Strategies for the Hydrogen Value Chain Page 24 Page 26